State of the Industry Report 2019: Food & beverage processing

Trends and fads may come and go, but what remains the same is the way cold food and beverage processors do business. Because let’s face it, catering to the ever-changing consumer can be a daunting task.

Rewind to Refrigerated & Frozen Foods’ 2014 State of the Industry report, and convenience, better-for-you, premium/indulgent and multicultural/global interests were key drivers of growth in the refrigerated and frozen foods sector.

While some of these trends still ring true, several market research firms bring to light new trends designed to heat up the chilled industry.

For example, the demand for frozen ready meals is expected to witness steady demands in the foreseeable future, according to research presented by Future Market Insights, Valley Cottage, N.Y., expanding at a CAGR of 4.3% and bringing in estimated revenue of over $47 billion. Frozen chicken meals will be a top-selling product in the overall frozen ready meals landscape.

The Food Institute, Upper Saddle River, N.J., tallied 527 food industry mergers and acquisitions (M&A) in 2018, down almost 11% from 2017’s record year, according to its annual report. Manufacturers, investment firms and retailers were once again the largest segments, taking part in more than half of the deals for the year. Food processors took part in 152 deals in 2018, a 19.4% decrease from 2017, while the retail sector increased almost 40% from the previous year. Acquisitions by restaurant companies in 2018 were relatively in line with the prior year. California was the most popular state for M&A activity.

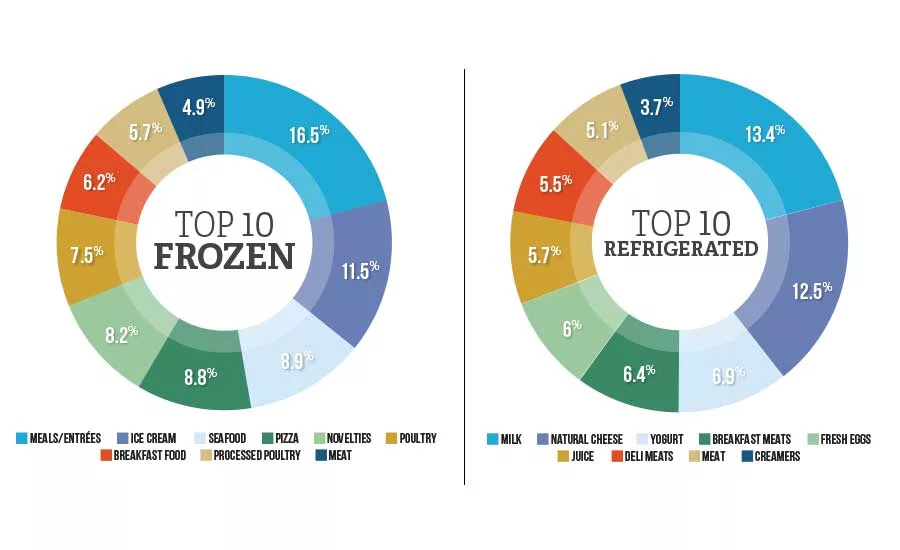

See the charts here!

Analysis of U.S. consumer spending and demographic patterns suggests significant changes for food and beverage operators and the real estate they occupy, including a greater push for convenient, prepared foods, a growing Millennial influence and the emergence of inner-ring suburbs as the industry’s hottest market, according to a report published by CBRE, Los Angeles.

Yet, despite an uncertain operating environment and continuing concerns about the availability of skilled labor, plans for new and expanded facilities are still on the horizon, according to a survey produced by Area Development, Westbury, N.Y. About 40% of the 118 corporate survey respondents say they plan to open new facilities within the next five years.

As retail undergoes significant change, private brands are setting the pace for the rest of the industry, as outlined in a study released by Daymon, Stamford, Conn. In 2018, there was a 4% increase in private brand sales, nearly six times the growth of national brands. That growth came from categories across the retail spectrum, including pet and food, among others. Private brands have also become a crucial source of differentiation, store choice and consumer preference, as research finds that 98% of national brand assortment is the same across retailers, 53% of consumers say they shop at a store specifically for its private brands and 81% buy private brand products on every shopping trip.

Specialty food sales outpaced the growth of all food at retail, up 10.3% vs. 3.1%, according to a report published by SFA. In fact, specialty food remains one of the fastest-growing segments of the food business. Fueled by increasing interest from both consumers and retailers, total sales jumped 9.8% between 2016-2018, reaching $148.7 billion last year.

Product innovation and the wider availability of specialty foods through mass-market outlets is playing a part in the industry’s success. Sales through foodservice represented 22% of sales, with retail taking the top spot with 76% of sales. While online represents less than 3% of sales, it has grown 41% since 2016.

The most successful brands focus on wellness, indulgence and convenience, according to an IRI report. For the first time, products developed by companies with annual revenues under $1 billion represented the majority of top-ranking brands, accounting for 51% of the products listed and representing 27% of Pacesetters revenues. Companies with sales between $1-5 billion continued to have declining representation, responsible for just 27% of products and 19% of revenues, as compared to 35% and 26%, respectively, five years ago. Larger companies, those with more than $5 billion in revenues, accounted for just 22% of Pacesetters products, but 54% of Pacesetters sales.

Despite a strong start to the year, consumer confidence dimmed at the end of Q1 2019, and is currently surging again due to a strong labor market. But, trade issues could easily cloud this outlook, according to another IRI survey. And, Millennials are outspending their older cohorts. In fact, younger Millennials’ edible dollar sales grew by 21.5% for March compared to a year ago.

Packaging presents eco-friendly alternatives

The food and beverage market accounts for more than 30% market share of biodegradable packaging market, according to a report released by Fact.MR, Rockville, Md. Paper and paperboard biodegradable packaging will retain its dominance in the biodegradable packaging market, as it may account for more than 95% of the total market revenue by 2028.

Meanwhile, product positioning, marketing, the economy, taste trends, business and consumer spending and the direction of the CPG sector all impact the future of packaging trends, according to insights released by L.E.K. Consulting, Boston, Mass. The vast majority of the brand executives (80%) interviewed said packaging is crucial to their brand’s success, and half (50%) said they expect to increase packaging spending over the next year. Nearly a quarter of that group (22%) said spending will go up by more than 10%. Nearly half of brand managers said that over the next five years, they’ll expand their “price-pack architecture” offerings. Think new refrigerator-friendly sizes of bottles and snack-size packages of certain foods. About 40% of brand owners said they’ve made changes toward sustainable packaging over the past two years, and the majority plan to move a portion of their packaging volume toward sustainable packaging options over the next five years.

In a separate study presented by L.E.K. Consulting, 57% of brand owners said they’re developing packaging that’s easier to open, 51% said they’re working on more single-serve package sizes and 49% said they’re stepping up placements in new distribution channels, such as convenience stores.

Furthermore, connected packaging, where multiple technologies enable brands to connect physical packaging to the virtual world, will become more commonplace in the global packaging industry in 2019 and beyond, as outlined in a trends piece by Mintel, Chicago.

And, as brands continue to expand into the e-commerce playing field, they will also need to establish an e-commerce packaging strategy, one that resolves how to produce more SKUs, smaller package sizes and quicker turnaround time. The Mintel report also discusses the plastic-free movement that many of today’s grocers are adopting, and brands must consider plastic-free packaging solutions that still claim appropriate shelf space.

See the charts here!

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

")